Fill Your Michigan Property Transfer Affidavit 2766 Form

When a piece of real estate changes hands in Michigan, an essential step in the process involves the filing of the Property Transfer Affidavit 2766. This legal document serves a critical function, alerting the local assessor's office to a change in property ownership. The timely submission of this form, specifically within 45 days following the transfer, is crucial to ensure compliance with state law and to avoid potential penalties. By accurately completing this affidavit, the new property owner provides the necessary information to update the public records, reflecting the sales price, the property's new ownership, and any exemptions for which the property may now qualify. This process not only facilitates a smooth transition of official documents but also plays a key role in determining the property's taxable value, thereby impacting the amount the new owner will pay in property taxes. The significance of the Property Transfer Affidavit 2766 in maintaining the integrity of the state's property records and in the overall administration of local property taxes cannot be overstated, making it an indispensable document in the conveyance process.

Document Sample

Reset Form

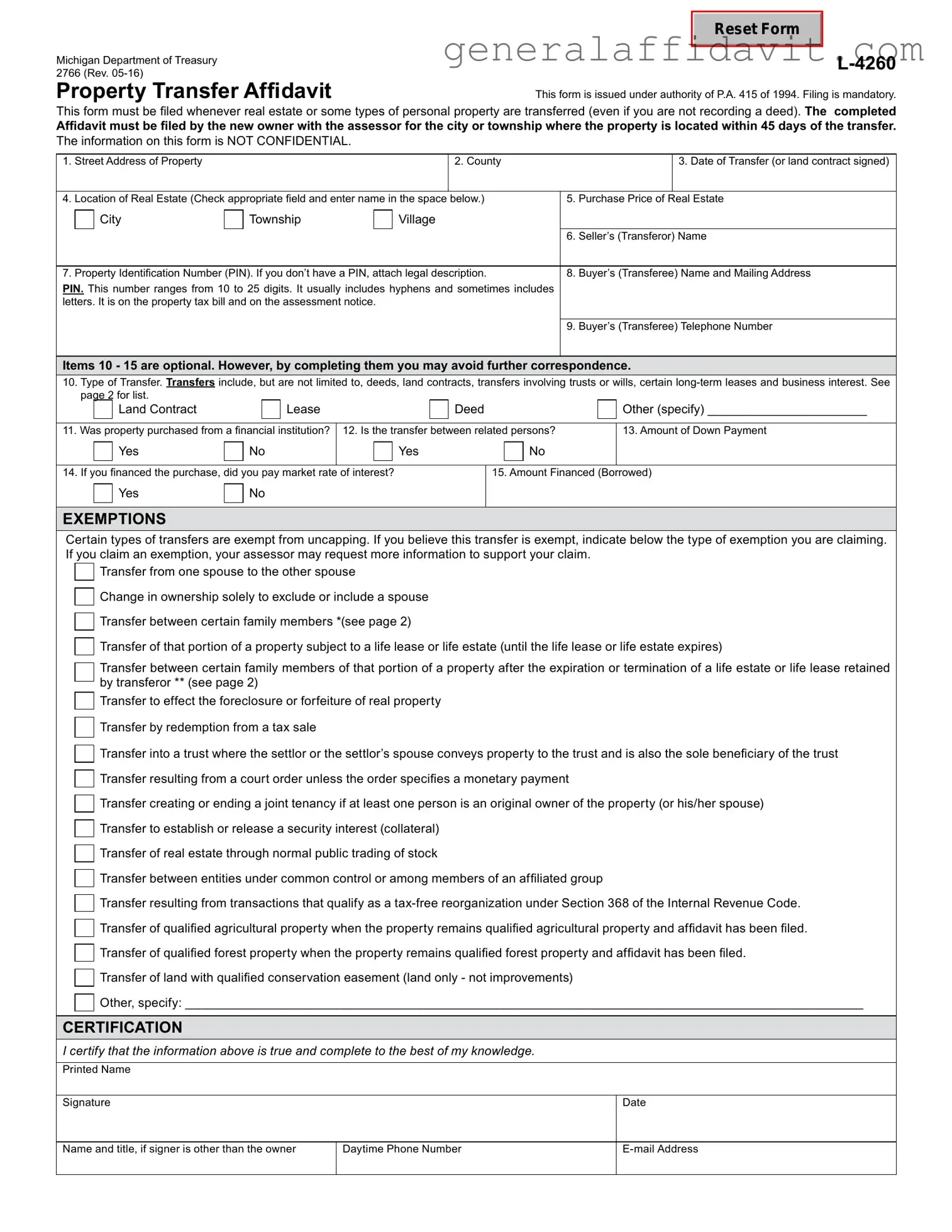

This form is issued under authority of P.A. 415 of 1994. Filing is mandatory.

This form must be filed whenever real estate or some types of personal property are transferred (even if you are not recording a deed). The completed

Affidavit must be filed by the new owner with the assessor for the city or township where the property is located within 45 days of the transfer. The information on this form is NOT CONFIDENTIAL.

1. |

Street Address of Property |

|

|

|

|

2. County |

|

|

3. Date of Transfer (or land contract signed) |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Location of Real Estate (Check appropriate field and enter name in the space |

below.) |

5. |

Purchase Price of |

Real Estate |

|||||

|

|

City |

|

Township |

|

Village |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

6. |

Seller’s (Transferor) Name |

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Property Identification Number (PIN). If you don’t have a PIN, attach legal description. |

8. |

Buyer’s (Transferee) Name and Mailing Address |

|||||||

PIN. This number ranges from 10 to 25 digits. It usually includes hyphens and sometimes includes |

|

|

|

|||||||

letters. It is on the property tax bill and on the assessment notice. |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Buyer’s (Transferee) Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

Items 10 - 15 are optional. However, by completing them you may avoid further correspondence.

10.Type of Transfer. Transfers include, but are not limited to, deeds, land contracts, transfers involving trusts or wills, certain

|

|

Land Contract |

|

|

|

Lease |

|

|

|

|

Deed |

|

Other (specify) _______________________ |

|||

|

|

|

|

|

||||||||||||

11. Was property purchased from a financial institution? |

12. Is the transfer between related persons? |

|

13. Amount of Down Payment |

|||||||||||||

|

|

Yes |

|

No |

|

|

Yes |

|

|

|

|

No |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|||||||||||

14. If you financed the purchase, did you pay market rate |

of interest? |

|

|

15. Amount Financed (Borrowed) |

||||||||||||

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS

Certain types of transfers are exempt from uncapping. If you believe this transfer is exempt, indicate below the type of exemption you are claiming. If you claim an exemption, your assessor may request more information to support your claim.

Transfer from one spouse to the other spouse

Change in ownership solely to exclude or include a spouse

Transfer between certain family members *(see page 2)

Transfer of that portion of a property subject to a life lease or life estate (until the life lease or life estate expires)

Transfer between certain family members of that portion of a property after the expiration or termination of a life estate or life lease retained by transferor ** (see page 2)

Transfer to effect the foreclosure or forfeiture of real property

Transfer by redemption from a tax sale

Transfer into a trust where the settlor or the settlor’s spouse conveys property to the trust and is also the sole beneficiary of the trust Transfer resulting from a court order unless the order specifies a monetary payment

Transfer creating or ending a joint tenancy if at least one person is an original owner of the property (or his/her spouse)

Transfer to establish or release a security interest (collateral)

Transfer of real estate through normal public trading of stock

Transfer between entities under common control or among members of an affiliated group

Transfer resulting from transactions that qualify as a

Transfer of land with qualified conservation easement (land only - not improvements)

Other, specify: __________________________________________________________________________________________________

CErTIfICaTION

I certify that the information above is true and complete to the best of my knowledge.

Printed Name

Signature

Date

Name and title, if signer is other than the owner

Daytime Phone Number

2766, Page 2

Instructions:

This form must be filed when there is a transfer of real property or one of the following types of personal property:

•Buildings on leased land.

•Leasehold improvements, as defined in MCL Section 211.8(h).

•Leasehold estates, as defined in MCL Section 211.8(i) and (j).

Transfer of ownership means the conveyance of title to or a present interest in property, including the beneficial use of the property. For complete descriptions of qualifying transfers, please refer to MCL Section

Excerpts from Michigan Compiled Laws (MCL), Chapter 211

**Section 211.27a(7)(d): Beginning December 31, 2014, a transfer of that portion of residential real property that had been subject to a life estate or life lease retained by the transferor resulting from expiration or termination of that life estate or life lease, if the transferee is the transferor’s or transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the transfer. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subdivision. If a transferee fails to comply with a request by the department of treasury or assessor under this subdivision, that transferee is subject to a fine of $200.00.

*Section 211.27a(7)(u): Beginning December 31, 2014, a transfer of residential real property if the transferee is the transferor’s or the transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the conveyance. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subparagraph. If a transferee fails to comply with a request by the department of treasury or assessor under this subparagraph, that transferee is subject to a fine of $200.00.

Section 211.27a(10): “... the buyer, grantee, or other transferee of the property shall notify the appropriate assessing office in the local unit of government in which the property is located of the transfer of ownership of the property within 45 days of the transfer of ownership, on a form prescribed by the state tax commission that states the parties to the transfer, the date of the transfer, the actual consideration for the transfer, and the property’s parcel identification number or legal description.”

Section 211.27(5): “Except as otherwise provided in subsection (6), the purchase price paid in a transfer of property is not the presumptive true cash value of the property transferred. In determining the true cash value of transferred property, an assessing officer shall assess that property using the same valuation method used to value all other property of that same classification in the assessing jurisdiction.”

Penalties:

Section 211.27b(1): “If the buyer, grantee, or other transferee in the immediately preceding transfer of ownership of property does not notify the appropriate assessing office as required by section 27a(10), the property’s taxable value shall be adjusted under section 27a(3) and all of the following shall be levied:

(a)Any additional taxes that would have been levied if the transfer of ownership had been recorded as required under this act from the date of transfer.

(b)Interest and penalty from the date the tax would have been originally levied.

(c)For property classified under section 34c as either industrial real property or commercial real property, a penalty in the following amount:

(i)Except as otherwise provided in subparagraph (ii), if the sale price of the property transferred is $100,000,000.00 or less, $20.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $1,000.00.

(ii)If the sale price of the property transferred is more than $100,000,000.00, $20,000.00 after the 45 days have elapsed.

(d)For real property other than real property classified under section 34c as industrial real property or commercial real property, a penalty of $5.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $200.00.

File Attributes

| Fact | Description |

|---|---|

| Purpose | The Michigan Property Transfer Affidavit Form 2766 is used to notify the local assessor's office of a transfer of real property. |

| Deadline | This form must be filed within 45 days of the property transfer to avoid penalties. |

| Governing Law | This affidavit is governed by the Michigan General Property Tax Act (Public Act 206 of 1893). |

| Filing Location | It must be filed with the local municipality where the property is located. |

| Required Information | Information needed includes the property's legal description, the transfer date, the part of the property transferred, and the value of the consideration for the transfer. |

| Penalty for Late Filing | If filed late, the transferor may face penalties up to a certain amount of the transfer tax imposed on the transaction. |

Guidelines on How to Fill Out Michigan Property Transfer Affidavit 2766

When a property changes hands in Michigan, the new owner must submit a Property Transfer Affidavit to the local assessor's office. This step is crucial for ensuring your property taxes are assessed accurately and reflects any changes in ownership. The Michigan Property Transfer Affidavit 2766 form is necessary for this process. Completing this form involves providing details about the property's sale and the parties involved. Here's a simple, step-by-step guide to help you fill out the form accurately.

- Begin by entering the date of transfer. This is the date when the ownership of the property was officially changed.

- Next, provide the address of the property in question, including the city, village, or township, along with the county and school district.

- Enter the property's tax identification number(s). This might include parcel numbers or any other identifier used by the local tax authorities.

- Fill in the name, address, and contact information of the new owner(s) — the grantee(s).

- For the section on the seller(s) or grantor(s), enter their name(s), address, and contact information.

- Provide the legal description of the property as recorded on your deed. This description might include lot numbers, subdivision name, and any other legal identifiers.

- Answer whether the transfer is exempt from real estate transfer tax and check the appropriate box indicating your reason if the transfer is exempt.

- If money exchanged hands during the property transfer, indicate the total consideration paid for the property, including both cash and the value of any mortgage assumed.

- Specify the type of transfer by checking the appropriate box, whether it's a conveyance of a deed, land contract, lease, or other.

- Confirm if the property will be used as the new owner’s principal residence by checking the corresponding box.

- Sign and date the affidavit at the bottom of the form. The new property owner, or an authorized representative, should provide their signature.

- Finally, submit the completed form to the local assessor's office. Check with the office for specific submission guidelines, such as whether it can be submitted by mail, in person, or electronically.

After submitting the Michigan Property Transfer Affidavit, the local assessor's office will review the details and adjust the property’s tax records accordingly. It’s a crucial step to ensure that property tax assessments reflect the current ownership and any exemptions the property may qualify for under the new ownership. Timely submission is important to avoid potential penalties and to secure any applicable tax benefits without delay.

Discover More on Michigan Property Transfer Affidavit 2766

What is the Michigan Property Transfer Affidavit 2766?

The Michigan Property Transfer Affidavit 2766 is a legal document required by the state whenever ownership of real estate is transferred. It notifies the local taxing authority, typically the city or township assessor, about the change in ownership. This form plays a crucial role in ensuring property taxes are assessed accurately and reflects the property's current market value and ownership status.

When must the Michigan Property Transfer Affidavit 2766 be filed?

This affidavit must be filed within 45 days of the property's transfer. If it is not filed within this timeframe, a penalty may be imposed. This penalty can amount to $5 per day for each day the filing is late, up to a maximum of $200. Timely filing ensures that property assessments and taxes can be updated to reflect the new ownership appropriately.

Who is responsible for filing the Michigan Property Transfer Affidavit 2766?

Typically, the responsibility falls on the buyer or the new owner of the property. However, anyone with a vested interest in ensuring the property's successful transfer, such as real estate agents or attorneys, can also file the affidavit on behalf of the owner. Regardless of who files it, it's vital that the information provided is accurate and complete to prevent any issues with the property's tax status.

What information is needed to complete the form?

To fill out the Michigan Property Transfer Affidavit 2766 correctly, you'll need various details about the transaction and the property itself. This includes the date of the transfer, the full names and addresses of the buyer and seller, the property's tax identification number, the sale price, and information regarding any exemptions claimed. Accurate and thorough completion of the form is necessary for a successful filing.

What happens after the form is filed?

Once the form is submitted, the local assessor will review the information to update the property's tax records. This can lead to an adjustment in the property's assessed value, which could impact property taxes. The change in ownership will also be officially recorded, which is essential for future transactions or inquiries about the property. It's a good idea to keep a copy of the filed affidavit for your records.

Where can I obtain the Michigan Property Transfer Affidavit 2766 form?

The form is available from the Michigan Department of Treasury's website, or you can pick up a copy at your local assessor's office. Some local offices might also offer an online submission option, making it easier to file the affidavit. Always make sure you're using the most current version of the form to avoid any problems with your filing.

Common mistakes

When property changes hands in Michigan, the law requires a completed Property Transfer Affidavit (Form 2766) to be filed with the local assessor's office. This document is critical in ensuring property taxes are assessed accurately and can greatly affect the new owner's tax obligations. However, mistakes during this process can lead to complications, delays, and possibly increased taxes. Here are nine common mistakes people make when filling out the Michigan Property Transfer Affid saidavit 2766 form:

- Not Filing On Time: The affidavit must be filed within 45 days of the transfer. Failing to meet this deadline can lead to penalties, including a fine.

- Incomplete Information: Leaving sections of the form blank can cause delays. The assessor's office needs complete information to process the transfer accurately.

- Incorrect Property Identification: The property's Parcel Identification Number (PIN) and legal description must match those on record. Errors here can misidentify the property, leading to incorrect tax assessments.

- Unsigned Form: An unsigned form is invalid. Both the buyer and the seller are often required to sign, depending on the local jurisdiction’s requirements.

- Failing to Specify the Transfer Type: The form requires specifying the type of transfer (e.g., sale, inheritance, trust transfer). Incorrect or missing information can affect the tax implications of the transfer.

- Incorrect Transfer Date: The true transfer date is crucial for tax purposes. Incorrect dates can lead to misapplied tax rates or penalties.

- Not Including Relevant Attachments: Sometimes, additional documents (like a copy of the deed or a death certificate, in the case of inheritance) are required. Failing to include these can stall the process.

- Miscalculating the Consideration Amount: The consideration amount (the total value exchanged for the property) must be accurately reported. Underestimating can lead to legal issues and penalties, while overestimating can unnecessarily increase the tax burden.

- Overlooking Local Requirements: Some local jurisdictions may have additional requirements or variations on the form. Not adhering to these local stipulations can result in the affidavit being rejected.

To avoid these common mistakes, it's wise to carefully review the entire form before submission, double-check all information for accuracy, and consult with a legal professional or the local assessor's office if there are any uncertainties. Accurately completing the Michigan Property Transfer Affidavit Form 2766 is essential for a smooth transfer process and to ensure the correct assessment of property taxes.

Documents used along the form

When dealing with property transactions in Michigan, the Property Transfer Affidavit 2766 form is an essential document. However, it's often just one part of the paperwork needed to ensure a smooth and legally sound process. Various other forms and documents typically accompany this affidavit to meet legal requirements and safeguard the interests of all parties involved. Let's explore some of these additional forms and documents that are frequently used alongside the Michigan Property Transfer Affidavit 2766.

- Warranty Deed: This document is used to transfer the title of real estate from the seller to the buyer. It includes assurances from the seller that the title is clear of liens or claims, providing the buyer with greater protection.

- Quit Claim Deed: Unlike a warranty deed, a quit claim deed transfers the owner's interest in the property without any guarantee about the title's clearness. It's often used between family members or to clear up a title issue.

- Title Insurance Policy: This insurance protects against losses due to defects in the title not discovered during the initial title search. It's a crucial safeguard for new property owners.

- Real Estate Transfer Tax Declaration (Form 2796): This form is used to declare the value of the property being transferred and calculates the transfer tax due, if any, based on the property's sale price.

- Homestead Exemption Form: If the property is the principal residence of the buyer, filing this form can provide a reduction in property taxes by exempting a portion of the home's value from taxation.

- Closing Statement: This comprehensive document outlines all the financial details of the transaction, including the sale price, loan amounts, closing costs, and the disbursement of funds. It’s vital for both buyer and seller to understand the financial aspects of the deal.

Together with the Michigan Property Transfer Affidavit 2766, these documents ensure a transparent and legally compliant transfer process. Each plays a specific role in clarifying the rights, responsibilities, and protections of the involved parties, contributing to a smooth property transition. Whether you're buying, selling, or simply adjusting ownership details, being familiar with these forms can significantly help navigate the procedural aspects of property transfers.

Similar forms

The Michigan Property Transfer Affidavit 2766 shares similarities with the Uniform Residential Loan Application. Both documents are essential in real estate transactions but serve different purposes. The Property Transfer Affidavit is a mandatory filing that alerts the local government to a change in property ownership, which could affect taxation. Conversely, the Uniform Residential Loan Application is used by prospective borrowers to apply for a mortgage. Despite their different applications, both require detailed information about the property and parties involved, ensuring that legal and financial entities have accurate records.

Another document akin to the Michigan Property Transfer Affidavit 2766 is the Seller's Disclosure Statement. This document is crucial in real estate transactions, where sellers are required to disclose the condition of the property to potential buyers. Like the Property Transfer Affidavit, the Seller's Disclosure Statement ensures transparency in the transaction process, providing important information that may affect the property's value and desirability. Both documents play a vital role in maintaining honesty and integrity in real estate dealings.

The Grant Deed is also comparable to the Michigan Property Transfer Affidavit 2766, as both are involved in the process of property transfer. The Grant Deed is used to officially transfer ownership from the seller to the buyer and guarantees that the property has not been sold to anyone else. Although the Property Transfer Affidavit does not convey ownership, it complements the Grant Deed by informing local government agencies of the ownership change for taxation purposes. Together, they ensure the transfer is legally recognized and properly recorded.

Finally, the Real Property Transfer Tax Declaration mirrors the Michigan Property Transfer Affidavit 2766 in its role in the documentation and taxation process during property transfers. This document is designed to calculate the tax owed on the transfer of property, based on the sale price or the property's current market value. While the Property Transfer Affidavit informs the local taxing authority of a change in ownership to reassess the property's value for taxation, the Transfer Tax Declaration directly involves the calculation and payment of taxes due as a result of the property transaction. Both are required for a legal and fiscally responsible transfer of property.

Dos and Don'ts

When filling out the Michigan Property Transfer Affidavit Form 2766, it's important to pay attention to detail and adhere to guidelines to ensure a successful submission. Below are some key do's and don'ts that can guide you through the process.

Do:- Read all instructions provided on the form carefully to ensure a complete and accurate understanding of the requirements.

- Use black ink when filling out the form to ensure legibility and to comply with scanning requirements.

- Ensure all information is accurate, including spelling of names, addresses, and legal descriptions of the property.

- Include the date of the transfer to accurately record when the property changed hands.

- Provide the tax identification number (TIN) or social security number (SSN) if required, as it is crucial for the processing of the affidavit.

- Sign and date the form in the designated areas to validate its authenticity.

- Double-check all entries for completeness and accuracy before submission.

- Contact local assessors or other relevant officials for clarification on any uncertain details or requirements.

- Keep a copy of the completed form for your records, as it may be needed for future reference or in case questions arise.

- Submit the form to the appropriate local government office, typically the assessor's office, in a timely manner following the transfer to avoid penalties.

- Leave any fields blank. If a section does not apply, mark it with “N/A” to indicate that it is not applicable.

- Use pencil or ink colors other than black, as this may affect the readability and scanning of the document.

- Guess on details. Ensure all information is correct and verifiable.

- Overlook any sections or instructions. Each part of the form has a specific purpose and requires attention.

- Forget to include contact information for follow-up if questions arise during processing.

- Submit the form without reviewing it for mistakes or omissions.

- Ignore local regulations or deadlines associated with property transfer affidavits, as these can vary.

- Omit the signature or date, as an unsigned or undated form is considered incomplete and invalid.

- Send the original form without making a copy for your records.

- Delay the submission of the form beyond the statutory deadline, which can lead to penalties or complications in the property transfer process.

Misconceptions

The Michigan Property Transfer Affidavit 2766 form is crucial in the process of property transfer within the state, yet many misconceptions surround its usage and requirements. Understanding these misunderstandings can help ensure compliance with Michigan law and smooth property transactions.

- Misconception 1: The form is optional.

Many believe filing the Michigan Property Transfer Affidavit 2766 is optional when it is, in fact, a legal requirement for all property transfers. Failure to submit this form can result in penalties.

- Misconception 2: It is only for the sale of property.

Contrary to common belief, this form is required for all types of transfers, including inheritance or gifting, not just the sale of property.

- Misconception 3: Only the buyer needs to worry about it.

Both the seller and the buyer have responsibilities in ensuring the form is completed and filed accurately and on time. It's a shared obligation.

- Misconception 4: It doesn't need to be filed if no money is exchanged.

Even if the property is transferred without money changing hands, as in a family inheritance or a gift, the affidavit still needs to be filed with the appropriate local government office.

- Misconception 5: Any errors can be easily corrected later.

While it's possible to amend the document, correcting errors can be a complex process that may delay property transfers or result in additional costs, emphasizing the importance of getting it right the first time.

- Misconception 6: It's the same as a deed.

Some confuse this affidavit with a property deed, but they serve different purposes. The affidavit notifies the local assessing officer of the transfer, whereas the deed is the legal document that transfers property ownership.

- Misconception 7: You need an attorney to file it.

While legal guidance can be helpful, especially in complex cases, it is not a requirement to have an attorney to file this affidavit. Property owners can complete and file the form themselves.

- Misconception 8: There's no deadline for filing.

There is indeed a deadline; the form must be filed within 45 days of the transfer. Late filings can result in penalties, including fees.

- Misconception 9: It applies only to residential property.

This form is required for the transfer of both residential and commercial properties, not just homes. Any real property transfer triggers the need for this affidavit.

Clarifying these misconceptions ensures all parties involved in property transfers are well-informed and compliant with Michigan's legal requirements, facilitating smoother transactions and preventing unnecessary complications.

Key takeaways

When it comes to understanding the process and requirements for filling out and using the Michigan Property Transfer Affidavit 2766 form, focusing on the key aspects can guide individuals through the procedure smoothly. Ensuring that all steps are followed correctly is critical for compliance with state law and for the efficient completion of property transfer documentation.

- Timeliness is Crucial: The form must be filed within 45 days of the property transfer. Failure to do so can result in penalties, including additional fees that may accrue over time.

- Mandatory for All Transfers: Any time property changes hands, regardless of the type of transfer, the Michigan Property Transfer Affidavit 2766 form is required by state law.

- Affected by Transfer Value: The information provided should reflect the true transaction value or the fair market value of the property at the time of the transfer, as this can affect tax assessments.

- Filing Location: The completed affidavit should be submitted to the local assessor's office in the municipality where the property is located, ensuring that it reaches the correct jurisdiction for processing.

- No Filing Fee: There is no charge for filing the affidavit, making it accessible for all parties involved in the property transfer.

- Accuracy is Essential: It is important that all information on the form is accurate and completely filled out to avoid processing delays or questions about the property transaction.

- Confirmation of Transfer: The affidavit serves as a formal acknowledgment of the property’s transfer and is an essential document for both the buyer and seller’s records.

- Impact on Taxes: Filing the affidavit promptly can ensure the property is assessed correctly for tax purposes and can prevent unexpected tax liabilities for the new owner. div>Note: Due to frequent updates to tax codes and local regulations, it's advisable to consult with a real estate professional or legal advisor to understand the current requirements and implications of the affidavit.